Case Study: 2x Earnings, 48% of Net Cash

A 1950's Buffett bargain in modern times.

Warren Buffett said he could earn 50% per year if he were managing $1 million.

I’m going to show you how he’d do it.

“I’d try to know everything about everything small.”

Conventional wisdom says markets are efficient. Gone are the days of Buffett scooping up businesses at 2x earnings or half of net cash.

I got news for you.

Conventional wisdom is wrong.

While markets are probably reasonably efficient for larger stocks, they’re wildly inefficient for smaller companies.

Here’s a quote from Buffett at the 2024 annual meeting:

I’m not making this claim. The GOAT is.

But I support the GOAT and I want to back him up.

So, I’m going to run a series of case studies from recent history. Things that have played out in the last 15 years or so.

We’re going to talk in depth about some 1950’s Buffett-style bargains.

And I’ll prove they still exist.

Case Study

Today we’ll observe the same stock at three different points in history.

At each point I believe shares were egregiously underpriced.

The business is called Pharmchem. Ticker: PCHM.

Before we begin, I don’t presently own this stock. I’m discussing the business from a historical perspective. This is not a recommendation to buy or sell shares. The stock is illiquid, and investors should take great care before transacting in such securities. I may buy or sell shares at any time in the future and have no intention of sharing those potential future actions with you or anybody else.

PCHM was formed in 1971 as a lab for integrated drug testing services. The company went public in 1992.

By 2002, the business had an accumulated deficit (negative retained earnings) of $10MM.

In 2004, the business delisted, stopped reporting and sold off assets.

By 2010, the business had sold off all its assets except for the Pharmchek sweat patch division. This division made a patch that was worn on the skin to test for drugs through the wearer’s sweat. It’s a pretty cool product.

In 2011, the company claimed it was unable to sell this final division due to its small size and regulatory complexity.

By 2013 the company had been dark for ~10 years.

And here’s where the fun begins…

Pharmchem 2013

Between September 2013 and May 2014, 3.6 million shares traded.

In that time, shares traded between $0.01 and $0.05 per share.

With 5.8mm shares outstanding, this would value the entire company at a maximum value of $290,000.

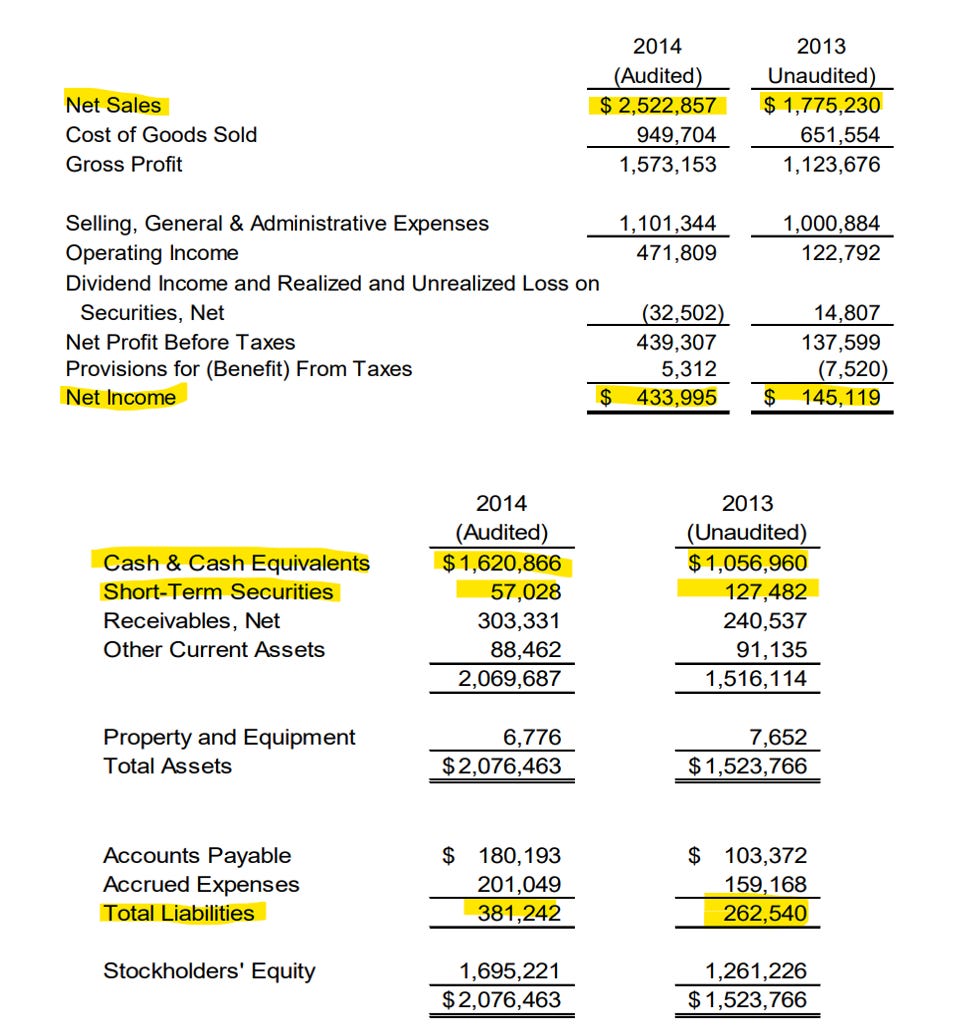

Here are the numbers from 2010 and 2012 (I don’t have 2011):

Buyers in 2013 were acquiring shares at 27% of net cash.

Revenues and profits were down in 2012, but the stock was still trading at less than 4x earnings.

It’s interesting, you can see SG&A growing as revenue shrinks, which is not what you want. But the price was still so far away from intrinsic value.

I like how consistent gross margins are. There are few small businesses that make a physical product that can continually earn 63% gross margins.

That fact alone ought to tell you there is something interesting here.

While we don’t have 2011 financials, it’s likely that the business earned a profit of ~$125,000 given the change in equity from 2010 to 2012.

Now, maybe the business was shrinking, or salaries were inflating. Maybe the business was subscale, and you don’t want to own it. There was no return of capital. It was just a growing cash box. That’s fair.

Of the 3.6mm shares traded from September 2013 to May 2014, I think most of them were exchanged in a block trade. But I believe an individual investor could’ve reasonably deployed $15,000 - $20,000 into the stock.

Let’s take a look at the company a few years later.

Pharmchem 2016

From April 2016 to November 2016, PCHM shares traded between $0.14 and $0.24/share.

This price range would value the company between $812,000 and $1,392,000.

During this time, 2014 and 2013 financials would’ve been available (2015 numbers didn’t come out until December 2016). Let’s have a look at the numbers:

Revenue grew 42% in 2014.

The stock was trading from 1.8-3.2x earnings.

The stock was priced anywhere from 48 - 83% of net cash.

A business with rapidly growing earnings was trading below its net cash.

1.1 million shares traded between April and November 2016. This represents $150-265k worth of dollar volume, depending on price paid.

Maybe one could reasonably expect to purchase $25-50k worth of the stock. Maybe more?

But again, the business continues to hoard cash. Management didn’t give a whole lot of insight. There weren’t quarterly earnings released. On top of that, you’d be completely alone in owning a stock like this. Zero chance anyone in your neighborhood also owns shares.

Pharmchem 2017

From December 2017 to July 2019 PCHM generally traded between $0.64 and $1.07/share (there were momentary spikes in price, but those were short-lived).

That price range valued the stock between $3.7MM and $6.2MM.

By December 2017 the business was paying a $0.05 annual dividend. Meaning shareholders were getting a yield ranging from 4.7% and 7.8%.

Here are the numbers that would’ve been available to investors beginning in December 2017:

Shares traded at a P/E ranging from 3.6 - 6.1x.

On an enterprise value basis, shares traded between 0.75x and 3.20x earnings.

Sales grew 29% in 2016 while net income grew 67%.

How It Played Out

Pharmchem’s business continued to grow nicely through covid.

By the end of 2020 the business was sitting on $7.8MM of net cash and had a profit of $1.9MM.

In 2021, some intelligent, honest investors took notice of PCHM, ran a proxy fight and kicked out the legacy management team.

Without getting into the details too deeply, this was a welcome win. Legacy management communicated poorly and tried to issue themselves huge stock awards. The group who came along in 2021 did shareholders a huge favor in replacing them.

The stock topped out at $5.50/share in 2021. Shares trade north of $3 today.

Observations

A PCHM buyer in 2013, holding to the peak in 2021, would’ve experienced a return ranging from 100-500x.

Now, you can say “Come on Dirt, that’s not fair. How would anyone have known about this company? Plus, you could only invest a few thousand dollars at a given time.”

That’s kind of the point.

These things exist because nobody works on them. Millions of shares traded back in 2013, so somebody must’ve figured it out.

But could a buyer really diligence PCHM? The annual reports were like 4 pages long, after all.

The answer is yes, you could diligence this company.

In fact, having less easily findable public information is to your benefit.

In the case of PCHM, there was a lot to be learned by calling on legacy management and pestering them. You could just show up at the office and ask to meet with someone.

You could figure out who some of the customers were by searching through county check registers on google.

You could find state level data on drug patch adoption in North Dakota.

And on, and on, and on.

You could call customers, former employees and other shareholders.

If you really wanted to, you could get the answers and build conviction in the story.

Again, a lack of information in the filings is to your benefit.

There is plenty of publicly available information hiding in plain sight.

Final Thoughts

PCHM represents a 1950-style Buffett investment.

A profitable, cash-rich business trading for an absurdly cheap valuation.

And this wasn’t 50 years ago. This all unfolded in the last dozen years.

Here’s the thing - I promise there is another PCHM type investment out there today.

There is some company cranking out earnings hand over fist while the market ignores it.

And in 2035, investors will look back and say, “well anyone would’ve bought that stock if they knew about it”.

Handicapping the PCHM’s of the world isn’t the hard part. It’s obvious when you see it.

The hard part is to find them.

You can run screens and read message boards all day long. Maybe that’ll work. But the best way to find cheap stocks is to get a list of every company on an exchange and go through it one by one.

“Start with the A’s” as Buffett said.

It worked in 1950.

It’ll work today.

DISCLAIMER: THIS IS NOT INVESTMENT ADVICE. I MAY OWN SECURITIES MENTIONED IN THIS ARTICLE. THIS IS NOT A RECOMENDATION TO BUY THIS STOCK OR ANY OTHER STOCK. I MAY BUY OR SELL ANY SECURITY AT ANY TIME. I MAY NOT TELL YOU IF AND WHEN I BUY OR SELL. THESE STOCKS ARE ILLIQUID AND YOU SHOULD UNDERSTAND THE IMPLICATIONS OF THAT IF YOU BUY THEM. THIS IS NOT TAX, LEGAL OR FINANCIAL ADVICE. I AM NOT YOUR FIDUCIARY. THIS IS THE INTERNET AND YOU’RE LISTENING TO A GUY NAMED DIRT.

Hi, I have an account with Interactive Brokers (Ireland) and they wouldn't let me invest in US small caps. Any europeans here managing to do so with IB or perhaps a different broker?

Very interesting dirt.

At the time, you would have needed to keep tabs on the company and receive/look for their annual letters:

https://s3.amazonaws.com/com-pharmcheck-cdn/document-uploads/2010-Letter-to-Stockholders.pdf?mtime=20190112103046

https://s3.amazonaws.com/com-pharmcheck-cdn/document-uploads/2012-Letter-to-Stockholders.pdf?mtime=20190112103047