Case Study: 3x Earnings, 20% of Net Cash, Repurchasing Stock

“Go look at every company on an exchange. Start with the A’s and don’t stop until you get to the Z’s. You’ll find a handful of interesting businesses. One or two will be absurdly cheap. Go learn everything you can about those one or two businesses.”

That’s how I normally answer the question.

It’s the question I’m most asked - “What’s your strategy? How do you find mispriced businesses?”

It’s probably a disheartening answer.

“Go spend a few thousand hours reading.”

That doesn’t really appeal to folks. But it’s also why good opportunities will never go away.

Almost nobody will do it.

The internet brought about ubiquity of information, but that didn’t kill market inefficiencies. The ability to screen on any metric you could possibly care about didn’t kill it. Artificial Intelligence won’t kill it either.

It’s like Robert Earl Keen said - the road goes on forever and the party never ends.

People will tell you the market is efficient.

They are wrong.

If you’re working with a small capital base, a halfway rational brain, and an endless supply of curiosity you will find inefficiencies.

I promise you they exist.

Case Study

My goal is to know a little bit about every profitable business in America beneath a certain size.

It was April 29th, 2022.

My strategy of “just read everything” led me to a little bank in Atlanta.

Citizens Bancshares Corpotation (Ticker: CZBS)

Up until April 2022, if you had asked me what I knew about CZBS I would have said something like this:

“Oh yeah, that’s the sleepy little bank in Atlanta. It’s probably traded around half of book value for years. Steady profits. It’s cheap, but I wonder if there’s ever a catalyst for value realization. I feel like it normally trades around 5-6x earnings.”

I would read Citizens’ annual report every year. Or at least skim it for 15 minutes to see what was going on.

On April 29th, 2022, the annual report was published. I popped it open and more or less saw the same business doing the same thing.

Discount to book, another solid year of profits, same old same.

But something caught my eye - it was this section of the balance sheet:

My first thought - “why the hell is Citizens issuing preferred stock?”

The bank had a loan-to-deposit ratio of 48%. It wasn’t like they needed more capital to fund loan growth.

The business had ample capital to meet regulatory requirements. It was already overcapitalized.

Citizens had a growth problem, not a capital problem. So why push common equity further down the stack?

It was just weird.

I jumped to the footnote on the preferred issuance:

So, Citizens issued noncumulative pref with a 1% rate?

Dirt’s not the sharpest tool in the shed, but even I understood the implication. CZBS raised $22MM of money that never had to be repaid. It would pay $220k in interest each year, but even that was noncumulative. So if CZBS missed an interest payment, it’s not like the interest would compound. It’s just deleted from history.

What the hell?

This preferred issuance isn’t an investment.

This is basically free money.

I read that paragraph like 10 times. Because I just assumed I must not understand what was happening.

Keep in mind, at this point CZBS had a market cap of $23MM. In effect, the business had been gifted an amount ($22MM) equal to its then stock price.

It would be like buying a house for $500k, walking in the front door, and finding $500k of cash laying on the floor.

I was dumbfounded.

Now I’m reading the whole report - every word. I’m thinking, man this is crazy.

I get to the end, and see this subsequent event footnote:

What is this?!

91 million dollars?

For what?

They say the money is non-dilutive. How’s that? No way these guys are about to get more sweetheart money.

I immediately hit the google machine to figure out what this “ECIP” thing is.

I get to the Treasury’s website and begin reading everything I can about the ECIP program.

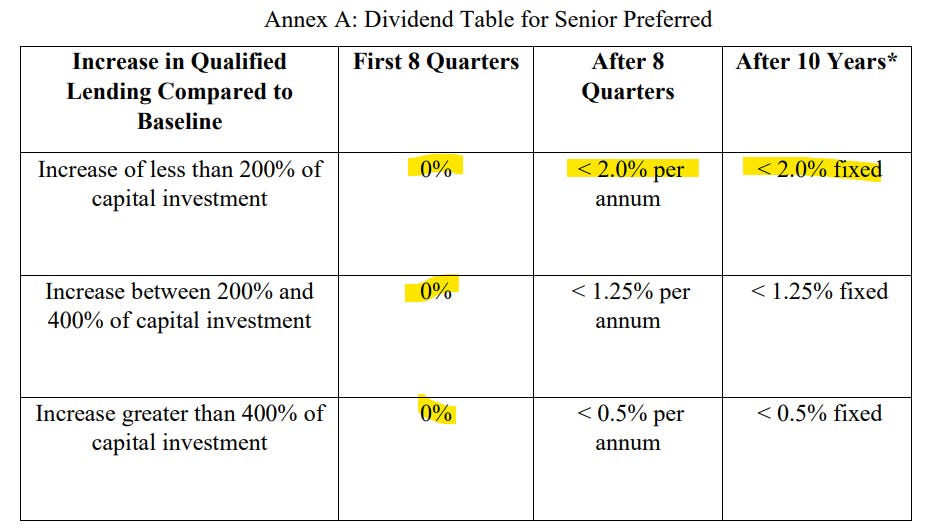

I make my way to this term sheet that highlights the key aspects of the investment. Here they are:

So CZBS was about to get $91MM of forever money, that would never have to be paid back. And it carried a noncumulative maximum rate of 2%?!

This too, is nearly free money.

Back to my house analogy:

This would be like buying a home for $500K, walking in the front door and finding $2,500,000 laying on the floor!

Am I Fucking Crazy?

I must’ve had a stroke. This can’t be right.

I keep reading.

Within 24 hours I’d decided that the money was real.

The first thing I did was try to figure out what person in their right mind “invested” $22MM into a bank and received 1% noncumulative prefs in return. I figured out the “investors” were large, money center banks.

I’d rather not go into detail as to why money center banks felt compelled to give $22MM of basically free money to Citizens. I think if you consider the social climate at the time, it ought to be somewhat obvious what was going on. This is not a political statement. I’m not opining on the merits of such an investment, and I’m not going to expand further. I’m just telling the story.

As to the $91MM of ECIP money. That was more or less the byproduct of the money printer going brrrrrr.

I began to think of ECIP as the apex of government stimulus. Covid broke the world for a brief moment, and lawmakers had to adopt all kinds of new tactics to get it back on its feet.

ECIP was an outcome of those tactics.

I began buying CZBS shares in early May. The funny thing is, up to this point I had never owned shares in a bank.

So I set out looking for someone to confirm that I wasn’t insane.

I reached out to some smart banking folks on twitter. By and large, they had no idea what I was talking about. They’d never heard of the program. They also had no historical precedent for which to frame the issue. It was totally out of left field. There was no paradigm.

Some folks were helpful, but most told me I must be mistaken.

I’d reach out to people who had mentioned the ECIP. I’d ask them questions and it was clear they hadn’t fully read the docs. They’d contradict statements that had clearly been spelled out in the purchase agreements.

Charlie Munger’s theory came to mind: “you have to know the other side’s argument better than they do themselves”.

Anyway, I just let these folks go. No need to introduce competition on the bid.

Then I took to calling banks themselves. I tried to speak to every company and banker that I could.

Banks that had accepted the ECIP money knew significantly more about the program than me. I remember one executive calling the ECIP “manna from heaven”.

Oddly enough, a buddy’s ex-girlfriend had a father that was the CFO for a CDFI bank in Mississippi. Mississippi was like mecca for ECIP money. So maybe this guy knew something.

So I call the buddy. He begrudgingly gives me his ex’s number. I give her a call and ask if I can meet her dad.

She’s kind of like “wait what do you want? when did we meet?”

Anyway, I finally get her dad, the CFO, on the line. And he’s a complete asshole.

He picks up the phone and his first words are “I have 5 minutes.”

The conversation went something like this:

CFO: “I have 5 minutes”

Me: “Uh hi, my name is Dirt. I’m an investor and I’m trying to learn about this ECIP program. Are you familiar with it?”

CFO: “No”

Me: “It’s this program where the government blows free money from the sky. It’s like PPP on steroids.”

CFO: "What? No. I don’t know anything about that.”

The call was over in less than 5 minutes. Then about an hour later my phone rings. It’s the asshole CFO.

CFO: “Hey I was looking into that ECIP thing. This is unbelievable. Would you be able to help us apply for the program?”

BINGO.

The Hunt Continues

There were ~200 banks that received this ECIP money. 12 of them were publicly traded. I studied each one.

My basic theory was, “let’s just invest in the bank that is least likely to do something stupid with this money”.

All these banks had won the lottery. And lottery winners go broke more often than the average citizen. I just didn’t want to hop into bed with the one that would blow it all up.

CZBS was probably the most prudent of the ECIP banks.

I read every call report as far back as I could. I got old annual reports. Management owned a nice chunk of stock and had been in place for over a decade.

Georgia had more bank failures than any other state during the GFC. CZBS managed through the GFC without booking a loss.

I figured Citizens must’ve been in the thick of it. If they could still earn a profit in that period, they must be shrewd capital allocators.

The bank had been in business for 100 years. And it earned a profit in 99 of those years.

Valuation

The valuation work was pretty easy.

CZBS earned ~$4MM in 2021. Rates were on the rise by Summer 2022. I figured CZBS could earn ~3% on its $113MM cash pile without taking any risk. Backing out the 1% due on the $22MM of money center pref, would result in ~$3.2MM of additional pretax earnings for the bank. Remember, ECIP had no cost in years 1 and 2.

Without taking any additional risk, CZBS could substantially increase net income.

But there were further considerations.

Citizens had taken in a bunch of cheap deposits in 2020-2021. I thought it was highly unlikely these deposits would flee or require material rate increases. Again, I’m not going to go into specifics. If you study the social climate it ought to be clear. Giant businesses were depositing funds with CZBS at near zero rates. That money was totally immaterial for these businesses, but incredibly material to Citizens.

With rates ripping upward, I figured there would be further upside in earnings as CZBS clipped a growing spread.

I didn’t get too cute with the valuation, however. I just thought it would be reasonably easy for the business to earn $6-7MM in 2022.

So, at a $23MM market cap, the business was selling for 3-4x earnings.

Reasonable Management

I didn’t need any heroes. I just wanted a management team that would act halfway intelligent.

I set out to understand the management team.

First, I had to give them credit for securing this equity capital and levering it up with cheap, stable deposits. There could be no better course to increase per share intrinsic value at that time.

The conservative balance sheet made me feel good, too. Citizens was extremely liquid and extremely solvent. They had obviously given up some potential profits to maintain this level of safety. I liked that.

The bank bought in ~5% of its stock in 2020. It repurchased more shares in 2021. I really liked that.

One thing that really impressed me was how CZBS handled the first $22MM it received from money center banks. Remember, they got that money in 2021. Think back to that period. The economic world had gone mad. Monkey jpegs, and hopeless businesses were given sky high valuations. People did all kinds of crazy stuff.

If ever someone were to lose his discipline, this would be the time.

CZBS got the $22MM investment and retained the vast majority of it at their parent company. Meaning, they didn’t downstream the cash to the operating business and immediately deploy it.

This capital was deposited into their own operating business, obviously. But I liked that the team got the money in a frothy moment and chose to do nothing. They treated that capital with great care.

I reached the conclusion that management was, at the very least, conservative. I’d later come to view them as good operators and capital allocators.

Dirtcheap Risk Assessment

I don’t know how any outsider can diligence a loan book. I know I sure as hell can’t.

Sure, we can see how loans are bucketed and all that. But you can’t really know the character of the borrowers, or if lending standards have changed. Lending is hard because poor choices don’t have immediate consequences. I think the best you can do is look at historical loan performance and try to understand how/if the approach has deviated in recent years.

So, aside from doing the obvious things, I was basically making a probabilistic guess.

The beauty of it was that there was room for enormous loan losses. Like, multiples worse than 2008. Citizens had been gifted so much money that it could take unprecedented losses and still be worth more than $11/share (in my opinion).

At some point, I stopped thinking of CZBS as a bank. CZBS was going to have a mountain of cash at its parent company in short order.

It wasn’t a bank. It was a holding company with $100MM of cash that happened to own a profitable bank.

And I could buy shares at a $23MM valuation.

That’s basically the story I’d tell myself every night.

Digging Deeper

I went back to the drawing board on the whole ECIP thing. The further down the rabbit hole I went, the more certain I became this was one giant grift… I mean gift.

When I first encountered the program, I considered ECIP money to be a set of golden handcuffs, or a golden coffin. Your bank would be made rich overnight, but you’d never be able to sell it. Because nobody in their right mind would buy out the Treasury’s pref at par.

“You can check out any time you like, but you can never leave.”

Turns out, the folks who concocted this program are a lot smarter than me. Treasury would sell its investment at some future point. And it would sell at fair market value. Importantly, when Treasury chose to sell, the issuer (Citizens) would have the first right of refusal to buy it back.

What’s fair market value for a noncumulative, perpetual pref that yields 2% max? Not much.

My lick-a-finger-and-stick-it-in-the-air DCF model told me fair value was ~20 cents on the dollar.

I just asked myself - “what kind of return would the median investor require to accept an optional stream of nonrecourse payments from a subscale bank?" I figured nobody in their right mind would take that deal, but if they had to, they’d want ~10%. So at a 2% yield, you’d pay 20 cents on the dollar.

I’m not smart enough for the galaxy brain vacuum math.

What was Citizens’ cost of equity? No idea.

Beta? Couldn’t tell you.

Equity risk premium? Still don’t know what that means.

Someone else can do all that highfalutin math, I’ll take the money.

This document (see page 19; released in March 2022) stated that shares could not be repurchased at less than 10 cents on the dollar. Which gave me further support that my 20% of face estimate was reasonable.

It turns out, fair value is somewhere between 7-28 cents on the dollar at today’s rates.

Back to the golden handcuffs - you could repurchase your own pref at some point in the future. Additionally, if you opted to sell your bank, Treasury would transfer its investment to the buyer (assuming the buyer was a CDFI/MDI). This obviously makes every ECIP recipient a potential takeover target.

How many banks would like to get their hands on 2% perpetual, noncumulative capital?

All these discoveries helped me see the program for what it truly was.

The Payoff

People started to realize what was going on in the Summer of 2022. The stock went from $11 to $20 in 3-4 months. By the end of the year, it was up to $28/share. Shares trade north of $50 today.

The ECIP trade was a life changing investment for me. I bought an absurdly large position (which would be laughably small to some others) and it worked.

But that’s not really the point of the story.

This isn’t a story about me.

This is a story about oddities that occur in public markets. There is no reason that a guy with average-at-best intellect should be able to find these kinds of opportunities.

Every document I sourced came from the public realm.

It didn’t require any sector expertise or superior intellectual horsepower. It required a laptop, an internet connection and endless curiosity.

Maybe you read this story and think I’m full of shit.

Maybe you’re right. Maybe I’m a lucky hick. Maybe markets are efficient.

Somedays, I’m not sure myself.

I do know this: I don’t want to wake up in 50 years to the shocking realization that all my perceived limitations were self-imposed. That I put a set of blinders on myself.

I’m going to keep doing what I love doing.

Chasing curiosity.

DISCLOSURE: THIS IS NOT INVESTMENT ADVICE. I MAY OWN THESE SECURITIES. I MAY BUY OR SELL THESE OR ANY OTHER SECURITIES AT ANY TIME. I MAY NOT TELL YOU IF AND WHEN I BUY OR SELL. THESE STOCKS ARE ILLIQUID AND YOU SHOULD UNDERSTAND THE IMPLICATIONS OF THAT IF YOU BUY THEM. THIS IS NOT TAX, LEGAL OR FINANCIAL ADVICE. I MAY MISSTATE CERTAIN FACTS UNKNOWINGLY. CERTAIN THINGS I SAY MAY TURN OUT TO BE INCORRECT. I AM NOT YOUR FIDUCIARY. THIS IS THE INTERNET AND YOU’RE LISTENING TO A GUY NAMED DIRT.

This is the post that made me subscribe. A no-brainer stock like this comes around very rarely and when it does it makes you question your sanity.

Written well too, made me laugh out loud a few times.

I remember when dirt dropped his initial Twitter threads on the ECIP program. As a “fingers and toes” real estate guy the obviousness of the hidden in plain site value struck me. I am thrilled that he since launched a paid substack