FitLife Brands Case Study

Cheap Stocks, Human Psychology and Dirt's Ego

In the past six months, I’ve written case studies about:

These five gentlemen have an average IQ that beats mine by more than I’d care to admit. But for some reason, people keep asking for stories from my own career.

So here you go.

Overview

April 1, 2022 was a Friday. I have my weekly golf match on Fridays. If you think I’m good at losing money in the stock market, you should see how efficiently I lose money on the golf course.

This Friday, however, I had to cancel my tee time.

I was about to walk out the door when I received a notification about a stock I’d followed for a couple years.

Fitlife Brands (Ticker: FTLF) announced that it would be delayed in filing its 2021 audit.

Here’s a section of the PR released that day:

Basically, the auditor had an issue with how particular sales were being recorded by the company. Should revenue be recognized when shipments leave Fitlife’s offices? Should it be recorded when it arrives at its destination? Is the company following internal controls around sales as stated in its policy?

The situation was vague, but uncomfortable.

My Background Owning FTLF (2020)

I originally bought FTLF, a health supplement provider, in the Fall of 2020. The stock was trading around 3.5x EV/FCF and it was run by shrewd operators that optimized for free cash flow generation. The CEO was properly aligned with shareholders. He’d also done an amazing job of saving the company after the failure of prior management.

GNC was FTLF’s largest customer at the time, representing ~75% of sales. GNC had just emerged from Chapter 11 bankruptcy. FTLF had earned a profit selling its products through GNC during a pandemic/bankruptcy, so I figured if there was money to be made in those trying times, it was likely the future would be at least as profitable.

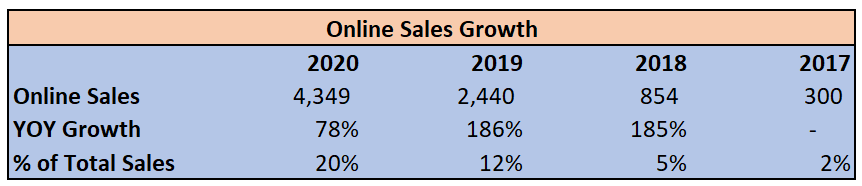

But the real beauty in the business lie elsewhere. FTLF had grown its online presence rapidly since the new CEO had taken over in early 2018:

Online sales carried significantly better gross margins than sales to GNC. There were two reasons why:

Online prices were higher than in store prices.

FTLF’s online sales occurred through Amazon. So there was no middleman (GNC) who needed a markup. Going directly to the consumer allowed FTLF to own more of the dollars spent by end customers.

I would later learn how much GNC franchisees enjoyed selling FTLF products. GNC earned a strong margin on in-store sales. This was a symbiotic relationship that allowed all parties to prosper.

I owned the shares for a while and later sold to go buy something else. But this was my general understanding as I entered the 2022 saga.

Back to April 2022

Markets were getting crushed in the first half of 2022. Investors were skittish. Couple that with the audit issues at FTLF and shares were down 35% from the end of 2021.

I was intrigued.

Having spoken with management on a few occasions in the past, I found them to be straightforward and honest. More than that, the actions of the company reflected the words of its leader.

So what was the issue?

Apparently, all revenue from GNC was being recorded the same way - when products were shipped. Certain orders should’ve had revenue booked at the time GNC landed the inventory at its warehouse.

So the issue is, should revenue be recorded today (when product leaves FTLF warehouse) or two days from now (when product is parked at GNC)? There was no question as to whether the revenue was real. Just a question about which day it should be booked.

My response - who cares?

We’re talking about a fraction of overall revenue here - a day or two worth of shipments.

Here’s another snippet of the April 1st PR:

Notice how tight the ranges are for expected performance over the year. Again, this is only a couple days of revenue in question.

I’ll also note the cash balance. The rest of the figures are estimates, but cash is stated as a fact. FTLF had $9.9MM of cash at year end. This is important because the business had no debt and no equity raises. Increases in cash could only be coming from profits. Cash had grown by $3.6MM for the year.

I was convinced that there were no operational problems inside FTLF. But investors were going to shoot first and ask questions later.

How Auditors Think

At this point in my career, I had spent more than 1,000 hours of my life with auditors. So I had a decent understanding of how they operate.

The vast majority of audits go off without any major issues. I’d guess it’s greater than 90%. There will be little hang-ups here and there, but nothing major. Auditors track every minute of their time. The main incentive is to get the job done on time and on budget. For these reasons, when something goes wrong, it takes a long time to get figured out. Problems tend to get escalated at the last minute because everyone wants to get the job done under budget, and because auditors aren’t used to dealing with major problems.

The other issue at hand was a deviation from FTLF’s internal controls. The fluctuation in sales and profits would be considered immaterial. But when it comes to internal controls, there is no concept of materiality. This is because an improperly operating control has the potential to cause material failures in a business.

For instance, if the quality assurance specialist at Company X marks outgoing orders as satisfactory without inspecting the shipment, there would be increased odds of mass product failures. Mass product failure = warranty claims = restated financials.

Long story short - I didn’t think this audit issue would get solved in a matter of weeks. The auditors were going to take a deep dive.

But the main questions and takeaways for an investor were as follows:

Did FTLF make a mistake? Technically, yes. But as a businessperson it really doesn’t matter. This was such a nonevent and had no bearing over management’s integrity or the intrinsic value of the business.

Was there any underlying issue in FTLF’s business? No.

Should the stock have fallen 35%? Hell no.

Incentives

“Show me the incentive and I’ll show you the outcome.” - Charlie Munger

My investment decision all boiled down to one question:

Had management behaved improperly?

So, let’s have a look at the incentives.

The CEO was an activist investor and fund manager. He had a strong history of helping companies behave in more shareholder friendly ways - not to mention his successful track record as an activist.

The CEO owned ~58% of the fully diluted share count between himself and his hedge fund. He bought nearly all his shares on the open market. If the CEO wanted to extract more money from the deal, he could’ve simply increased his salary. There was plenty of cash on the balance sheet to do so. He had voting control over the business. He could’ve enriched himself a dozen different ways, and he chose not to.

Any implication of channel stuffing would be absurd. There was no analyst coverage for this business. Revenue moving up or down by 1% would have almost zero impact on intrinsic value. It’s not like the CEO could sell a material amount of stock on a good earnings report.

Basically, I thought the management team were hardworking, honest folks.

Valuation

Between April 1st and June 30th 2022, I bought shares at an average price of $10.63.

Dayton Judd became the CEO in February 2018. The financials show how well he expanded margins and managed SG&A.

I had a rough estimate of where free cash flow may come in for 2022. My expectation ended up being high, but this is what I believed would happen at the time.

Strength of Management

FTLF was cheap. But the real power of the business was in the management team.

After Dayton Judd took the reigns in early 2018 the business became significantly more profitable. There are very few exceptional managers in the microcap space. Dayton is one of them.

What’s most impressive is that his strategy was so simple. Focus on the products that earn a satisfactory margin, and don’t waste money on unnecessary expenses. He wasn’t afraid to see revenue shrink if it resulted in more free cash flow.

FTLF repurchased 20% of its outstanding shares between 2018-2019.

Dayton’s goal was to find other supplement businesses for FTLF to buy. He was incredibly disciplined through the frothy markets of 2020 and 2021. FTLF made one small acquisition in 2021, buying Nutrology for ~1x forward earnings.

This CEO was a capital allocator’s dream.

The supplement space is rife with bloated companies. Giving Dayton Judd a fistful of cash to go buy supplement businesses is like staking Phil Ivey in a poker match against your drunk buddies.

How It Played Out

Fitlife was unable to provide Q’s or K’s until October 2022. Investors received a brief quarterly update which shed light into how the business was doing.

Fitlife had to restate financials back to 2019. The restatements were minor, with net income changing by less than 5% in each year. The sum total of the change in cumulative net income between 2019 and 2020 was $23,000. It was a joke.

I should buy the old auditor a nice bottle of wine. They gave me a great buying opportunity.

FTLF would go on to complete two major acquisitions in 2023. The business uplisted to Nasdaq. Here’s how shares have moved since - the red line represents the period in which I was buying:

Final Thoughts

I made a little money in Fitlife. But I’m not any kind of hero in this story. In fact, Fitlife taught me a valuable lesson.

I knew enough to understand how good this management team was. But some shiny object pulled me away. I should’ve never sold the shares I originally purchased in 2020. Those shares would’ve increased by 530% by now.

Additionally, I sold my 2022 shares too soon. I was patting myself on the back the whole way - “way to go Dirt, you made a profit here again! You’re so smart!” See me, pictured below:

I should have just held my shares.

If I have a strong management team that’s aligned with my interests and a stock that is consistently undervalued, there is no reason to sell. I’m not a FTLF shareholder anymore, and I haven’t been for most of 2024. Ouch.

The FTLF case is interesting. It goes to show how you can profit in small companies. I don’t think shareholders were considering the implications of the delayed audit and what was really going on inside the business. Folks saw the headlines and immediately wanted to exit.

It didn’t take a Master’s Degree in human psychology to understand how this management team was incentivized. And it didn’t take a PhD in accounting to understand that the revenue accrual issues had zero impact on the intrinsic value of the business.

Sometimes Mr. Market throws you a fat pitch. Maybe next time I’ll keep rounding the bases instead of sliding head first into second.

DISCLOSURE: THIS IS NOT INVESTMENT ADVICE. I MAY OWN THESE SECURITIES. I MAY BUY OR SELL THESE OR ANY OTHER SECURITIES AT ANY TIME. I MAY NOT TELL YOU IF AND WHEN I BUY OR SELL. THESE STOCKS ARE ILLIQUID AND YOU SHOULD UNDERSTAND THE IMPLICATIONS OF THAT IF YOU BUY THEM. THIS IS NOT TAX, LEGAL OR FINANCIAL ADVICE. I AM NOT YOUR FIDUCIARY. THIS IS THE INTERNET AND YOU’RE LISTENING TO A GUY NAMED DIRT.

FTLF is a great turnaround story with new management. Glad to see your thought process at the moment, as well as your reflection on what went right and what went wrong (selling too soon). Another core Dan Smoak and Dave Waters memory for me, now with Dirt’s perspective!